Paying international suppliers is one of the highest-volume payment tasks most finance teams manage. Unlike employee payroll, which runs on a fixed cycle, supplier payments follow purchase orders, invoice terms, and delivery schedules. These vary across dozens or hundreds of supplier relationships at once.

The cost of getting this wrong is real. Late supplier payments damage trading relationships and can trigger penalty clauses. Opaque FX pricing quietly erodes margins on every transaction. A manual payment process that works at 50 suppliers breaks down at 500.

This guide covers how to pay international suppliers efficiently, how to manage FX costs across variable volumes, and what compliance obligations apply. It also covers your compliance obligations and what to look for in a payment provider as your supplier base scales.

If you also pay employees or contractors overseas, we have dedicated guides covering both. Our guide on paying international employees and our guide on paying international contractors cover each in detail.

Why paying international suppliers is operationally complex

Supplier payments look simpler than payroll on the surface. They carry no employment compliance obligations or tax withholding requirements in most cases. No statutory deadlines tie to an individual’s livelihood. In practice, however, supplier payments at scale create their own set of operational pressures.

Volume and variety

A business with 200 international suppliers may be managing payments across 30 currencies, 15 payment methods, and a dozen different banking relationships. Each supplier has its own payment terms, invoice format, and bank account structure.

Some suppliers require payment via SWIFT, while others use local payment rails. Furthermore, certain currencies carry additional compliance requirements.

At low volumes, the variety is manageable with manual processes. As supplier numbers grow, the manual overhead compounds quickly. A finance team processing 500 international supplier payments a month cannot do so efficiently without structured payment infrastructure.

Payment terms and cash flow timing

Supplier payment terms vary widely. Net 30, Net 60, and 90-day terms are common in international trade, alongside early payment discounts for prompt settlement. Managing these terms across a large supplier base requires clear visibility of what is due and when, across multiple currencies.

Late payment to suppliers is not just a relationship risk. In some jurisdictions it carries legal consequences. In the UK, the Late Payment of Commercial Debts (Interest) Act 1998 gives suppliers the right to charge interest on overdue invoices. Finance teams need systems that surface upcoming payment obligations before they become overdue, not after.

The true cost of paying international suppliers

Most businesses know what they are paying their suppliers, but fewer know what it is costing them to make those payments. The true cost of international supplier payments includes the FX margin applied on each currency conversion, correspondent banking fees deducted in transit, and the staff time consumed by manual payment processing and reconciliation.

Take a business making 300 international payments a month at an average of £10,000 each. A 1.5 per cent FX margin on those payments amounts to £45,000 in annual FX costs. As a result, many businesses overlook this cost because it sits within the exchange rate rather than appearing as a separate fee.

Compliance requirements for paying international suppliers

Supplier payments carry fewer compliance obligations than employee or contractor payments in most jurisdictions. However, several requirements do apply, and overlooking them creates financial and reputational risk.

Sanctions screening

Every international payment must be screened against sanctions lists before it is released. Sanctions are restrictions imposed by governments and international bodies that prohibit financial transactions with certain individuals, entities, and countries. In the UK, the relevant lists come from the Office of Financial Sanctions Implementation (OFSI), part of HM Treasury.

OFSI is the UK authority responsible for implementing and enforcing financial sanctions. Making a payment to a sanctioned entity, even unknowingly, can result in significant penalties. In most cases, payment providers carry out sanctions screening automatically. Finance teams should confirm this with their provider and understand what happens when a payment is flagged.

Anti-money laundering obligations

Businesses making large or unusual international payments have obligations under anti-money laundering (AML) regulations. AML is the legal framework designed to prevent financial crime. It requires businesses to identify and verify the parties they transact with. In practice, this means knowing who you are paying and ensuring funds are used for legitimate purposes.

This includes maintaining accurate supplier records, conducting due diligence on new suppliers before making first payments, and flagging unusual payment patterns for review. That said, the specific requirements vary by industry and jurisdiction.

VAT on international supplier invoices

The VAT treatment of payments to international suppliers depends on where the supplier is based and the nature of the goods or services provided. For UK VAT-registered businesses receiving services from overseas suppliers, the reverse charge mechanism typically applies.

Under the reverse charge, you account for the VAT on the supplier’s invoice rather than the supplier charging it to you. For VAT-registered businesses, this is not usually a cash cost. It does, however, create a reporting obligation and affects your VAT return. Consequently, getting this wrong can result in penalties and interest.

Transfer pricing for intercompany supplier payments

Businesses that pay suppliers within their own group face additional compliance requirements around transfer pricing. This applies whether you are a UK subsidiary paying a parent company or an overseas affiliate.

Transfer pricing rules require you to conduct intercompany transactions at arm’s length. This means pricing them as you would with an unrelated party.

This is a complex area of international tax law and is most relevant to larger groups with significant intercompany payment flows. HMRC provides guidance on transfer pricing obligations for UK businesses.

How to pay international suppliers step by step

The operational flow for paying international suppliers shares some characteristics with paying international contractors but differs in important ways. Volumes are typically higher, payment terms are more structured, and the relationship between payment and goods or services received is more formal.

Step 1: Purchase order and invoice matching

A well-run accounts payable process starts before the invoice arrives. You raise a purchase order (PO) when engaging a new supplier, capturing the agreed price, currency, quantity, and payment terms. When the supplier’s invoice arrives, you match it against the PO.

Three-way matching compares the PO, the invoice, and the goods receipt note. It is the standard control for ensuring payment is only made for goods or services that were ordered and received. This step is often manual in smaller businesses and automated in larger ones through ERP (Enterprise Resource Planning) systems.

Step 2: Approval and payment instruction

Once an invoice is matched and approved, your team instructs it for payment. For international payments, this means selecting the payment method, confirming the currency, and initiating the transfer. A maker-checker control is standard practice for high-value international transfers. This is when one person raises the payment and a second authorises it before release.

Payment terms determine when the payment should be released. A Net 30 invoice received on 1 Jan should be paid by 31 Jan. Managing this across hundreds of suppliers requires either a structured payment run schedule or an automated payment scheduling system.

Step 3: Currency conversion

If the supplier invoices in a foreign currency, conversion from your home currency happens either at the point of payment or in advance. Supplier payments are often less predictable in timing than payroll but more predictable than contractor invoices. Agreeing payment terms upfront helps with planning.

If you pay suppliers regularly in the same currency, consider holding a balance in that currency. It reduces the number of individual conversions and gives you more control over when you convert. For larger or less frequent payments, the FX strategy depends on your treasury policy and the volatility of the currencies involved.

Step 4: Payment execution

The payment is released through your payment provider using the appropriate payment method for the destination country and currency. The table below sets out the main options.

| Payment method | Coverage | Speed | Cost | Suitable for |

|---|---|---|---|---|

| SEPA Credit Transfer | 36 European countries (EUR only) | Same or next business day | Low | Euro supplier payments within Europe |

| SEPA Instant | Growing coverage across Europe | Seconds | Low to moderate | Time-sensitive euro payments where supported |

| Local payment rails | Varies by country | Same day in many markets | Low to moderate | High-volume payments in supported markets |

| SWIFT | Global | 1 to 5 business days | Moderate to high. Correspondent fees may apply. | Markets without local rail access |

Settlement times and costs vary by provider, corridor, and the currencies involved. For high-volume supplier payment programmes, the choice of payment method has a meaningful impact on both cost and supplier experience.

Step 5: Reconciliation

Once payments are released, each transaction needs to be matched against the corresponding invoice in your AP system. To reconcile at scale, you need structured transaction data from your payment provider. This should include the payment reference, exchange rate, settlement date, and beneficiary details.

Without this data, reconciliation is a manual, time-consuming process. This creates end-of-month pressure and leaves errors undetected for longer than they should be.

Managing FX costs for international supplier payments

FX cost management is more important for supplier payments than for any other payment type covered in this guide. Higher volumes and greater frequency mean the cumulative impact of a poorly managed FX programme is significant. A systematic approach to supplier FX is one of the highest-return improvements a finance team can make.

Understanding the true cost of FX when paying international suppliers

When you convert currency to pay a supplier, the cost is not always visible as a line item. Most payment providers and traditional banking providers apply a margin to the exchange rate. This means you convert at a rate that is less favourable than the rate at which the provider traded. The difference is the provider’s revenue on the transaction.

A margin of 1.5 per cent sounds modest. On a monthly programme of £500,000 in foreign currency conversions, that is £7,500 per month or £90,000 per year. Finance teams that track FX costs explicitly find the savings from switching to a more transparent provider are material. Most absorb these costs into general payment costs without realising.

Spot versus forward contracts for paying international suppliers

Most supplier payments are made at the spot rate, meaning you convert at the rate available at the time of payment. For suppliers paid regularly, in predictable amounts, there is a case for using forward contracts to lock in rates ahead of payment dates.

A forward contract is an agreement to convert a set amount of currency at a pre-agreed rate on a future date. For a business with significant recurring supplier payments in volatile currencies, forward contracts can provide meaningful cost predictability. Whether they are appropriate depends on your treasury policy and risk appetite. Seek independent professional guidance where needed.

Holding multi-currency balances

If you pay multiple suppliers in the same currency, holding a balance in that currency avoids repeated conversions and reduces your exposure to short-term rate movements. A multi-currency account lets you receive funds, hold them, and pay suppliers in the same currency without converting back and forth.

This is particularly useful for businesses importing from a single region where most suppliers invoice in the same currency. Holding euros or US dollars and paying suppliers directly from that balance simplifies both the FX process and the reconciliation.

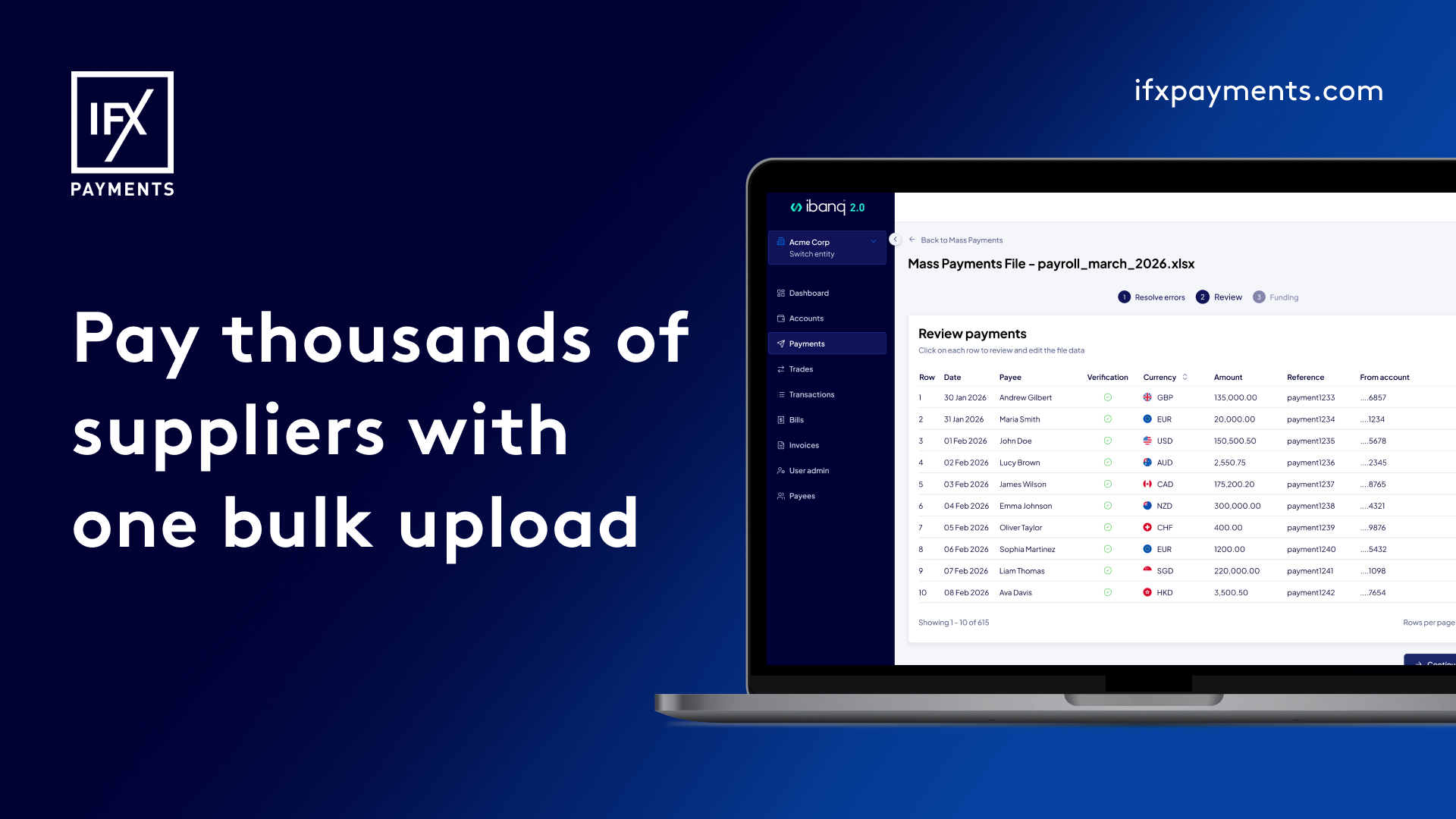

Bulk payment runs and FX efficiency

Processing supplier payments in bulk rather than individually has FX advantages as well as operational ones. A single conversion of £200,000 to USD to fund a batch of supplier payments is typically more efficient than 20 individual conversions of £10,000 each. Bulk conversions give you a single rate to track and a single reconciliation entry. Furthermore, your FX provider may also offer better pricing on larger transaction sizes.

This requires a payment platform that supports bulk file uploads and mass payment processing. If you are instructing payments individually through a banking portal, the operational and FX efficiency gains from batch processing are not accessible.

Common mistakes when paying international suppliers

The most common problems when you pay international suppliers are predictable. They tend to emerge as supplier numbers grow and the informal processes built for a smaller supplier base stop working.

Poor supplier onboarding for international payments

The quality of your supplier payment data determines the reliability of your payments. Incorrect IBANs, mismatched beneficiary names, outdated bank details, and missing SWIFT codes all cause payment failures and delays.

Supplier onboarding is the process of capturing and verifying banking details before the first payment. It is often treated as an afterthought. It should be treated as a control.

A structured onboarding process, with a confirmation step where new banking details are verified before being added to your payment system, reduces the risk of misdirected payments. For first-time payments above a certain value, call-back verification is standard practice. This is where a team member confirms new banking details directly with the supplier by phone.

No visibility of international supplier payment costs

Finance teams that cannot see the FX margin applied to each conversion cannot manage it. If your payment provider does not disclose the rate margin at the point of instruction, or if FX costs are rolled into a blended payment fee, you are operating without cost visibility on a significant line item.

Ask your provider to confirm the margin on each conversion separately from any transaction fee. If they are unwilling to do this, that is a signal worth taking seriously. Transparent FX pricing is a baseline expectation for any specialist payment provider.

Fragmented payment infrastructure

Businesses that grow internationally often end up with supplier payments split across multiple banking relationships, each covering a different region or currency. This fragmentation creates reconciliation complexity and makes it harder to negotiate better FX terms. It also increases the risk of payments falling through the gaps between systems.

Consolidating supplier payments into a single platform, or as few as operationally justified, reduces manual data movement and gives finance teams a single view of all outgoing payments. This does not always mean switching providers immediately. It can mean starting with the highest-volume corridors and consolidating incrementally.

Manual payment runs at scale

Instructing supplier payments individually through a banking portal is practical for a handful of payments. At 100 or more international monthly payments, it becomes a meaningful operational burden and a source of keying errors. A payment platform that supports bulk file upload, where a single file containing all payment instructions is uploaded and processed simultaneously, removes both problems.

Automation of recurring supplier payments, where payment terms and beneficiary details are held in the system and payments are scheduled automatically, further reduces manual effort and the risk of missed payment deadlines.

Treating international supplier payment reconciliation as an end-of-month task

Reconciling supplier payments after the fact concentrates significant effort at month end. Errors, duplicate payments, and FX discrepancies accumulate rather than being caught immediately. A payment provider that produces structured, exportable transaction data at the point of execution makes real-time or near-real-time reconciliation practical.

Integrating payment data directly into your ERP or accounting system removes the reconciliation bottleneck. It also reduces the risk of errors introduced by manual data re-entry.

Choosing a payment provider for international supplier payments

The requirements for paying international suppliers at scale are more demanding than for employees or contractors. Volumes are higher, the range of currencies and corridors is wider, and consequently the operational efficiency gains from getting the provider choice right are larger.

Currency coverage and local payment rails

Confirm that your provider can pay out in the currencies your suppliers invoice in. A provider with direct access to local rails in your key supplier markets will be faster and more cost-effective than one routing all payments through SWIFT. For businesses with significant supplier bases in Europe, Asia, or the Middle East, local rail coverage is a meaningful differentiator.

Transparent FX pricing

For supplier payments, FX pricing transparency is more important than for any other payment type. Ask any prospective provider to confirm the margin applied to each conversion, stated separately from transaction fees. The ability to see the rate at the point of instruction, rather than discovering it in reconciliation, is a basic requirement for managing your FX programme effectively.

Bulk payment and mass payment capability

For businesses with significant supplier bases, bulk payment processing is non-negotiable. Your provider must handle large batches of payment instructions from a single file upload. Look for a platform that supports bulk file ingestion in standard formats and provides real-time payment status updates. It should also handle exceptions cleanly without manual intervention for each failed payment.

Supplier onboarding and beneficiary management

Managing a large supplier beneficiary list requires a platform that supports bulk uploads, version control for updated banking details, and a clear audit trail for every change. Notably, supplier banking details change more frequently than most finance teams expect. A provider that makes it easy to update and verify beneficiary information reduces the risk of misdirected payments.

Integration with your AP system

The most efficient supplier payment operations integrate the payment platform directly with the AP or ERP system. This allows approved invoices to flow through to payment instruction without manual re-entry. API (Application Programming Interface) access is typically how this integration works. An API is a connection point that allows two software systems to exchange data automatically.

Not every business needs full AP integration. However, for businesses processing more than a few hundred international supplier payments per month, the operational savings from automating the data flow between systems is significant.

Payment controls and audit readiness

Supplier payments are high-value and frequent. Maker-checker approval workflows, role-based access controls, and a complete payment audit trail are governance requirements, not optional features. Any provider that cannot demonstrate these clearly during a sales conversation should not be handling your supplier payment programme.

Getting the foundations right

Paying international suppliers well is a sign of a well-run finance operation. The complexity is real, particularly at scale, but it is also well understood. The payment infrastructure and FX tools available today make it possible to pay suppliers in most currencies, on time, with full cost visibility and a clean audit trail.

If your supplier payment programme has outgrown your current process, it is worth reviewing your approach. In addition, reducing the FX costs embedded in your existing setup is another reason to do so. In turn, the gains from getting this right compound with every payment run.

At IFX Payments, we work with businesses managing high-volume international supplier payments across multiple currencies and corridors. We are an FCA-regulated Electronic Money Institution (EMI), authorised under the Electronic Money Regulations 2011 (FRN 900517).

Through our ibanq platform, we provide multi-currency accounts, transparent FX pricing, bulk payment processing, alongside the approval controls and reconciliation data that finance teams need to manage supplier payments at scale. If international supplier payments are a growing challenge for your business, we would be glad to talk through how we can help.

The contents of this article do not constitute financial advice and are provided for general information purposes only. Links to third-party websites are included for convenience only, and IFX Payments holds no responsibility for the content, services, products, or materials on those sites. All testimonials, reviews, opinions or case studies presented on our website may not be indicative of all customers. Results may vary and customers agree to proceed at their own risk.